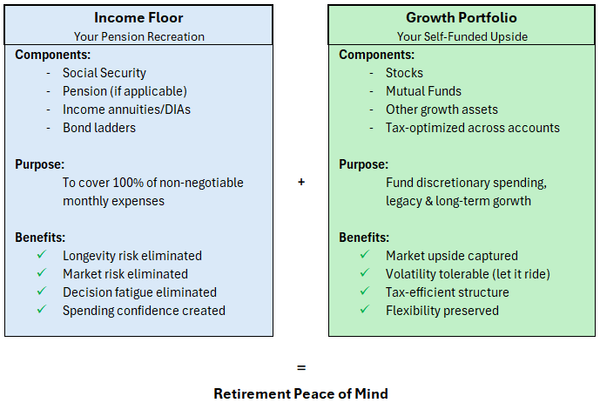

Build the Floor First

The Income Floor Effect

The Income Floor Effect

Every spring, I sit down with a stack of tax returns. My clients are mostly retirees or people within a few years of retirement. By now, I’ve reviewed enough 1099s and IRA statements to spot the patterns before I even get to the numbers. Most of my clients did

The hidden return nobody measures, and why it may be your most valuable asset

Most retirement anxiety is not about a specific threat. It is about a cloud.

*Before we begin, this week’s piece is shorter than usual due to the end of tax season and other demands. I wanted to ensure it was worth your time. People tell me retirement planning is hard because it is complicated. The tax rules are confusing. Social Security has more

The hardest part about retirement taxes is that they usually become important long before they become visible.

The market didn't change. Your relationship to it did.

Why the calmest stretch after you stop working often sets up the biggest pressure later

Why a large portfolio doesn't automatically create peace of mind, and why structure matters more than size

A new client sits down for their first retirement planning meeting. Before discussing income needs, taxes, or what they actually want from retirement, the advisor hands them a questionnaire. It asks questions like: How would you react if your portfolio dropped 20%? Would you prefer stability or growth? What level

The difference between feeling safe and actually being secure

The three-layer system that removes the need to depend on markets cooperating at exactly the right time

investment portfolio

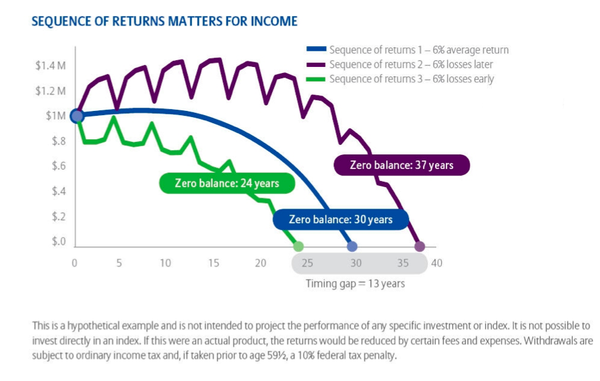

Why the real risks show up in years 10 to 25 and how to keep income steady for 30 years

annuity

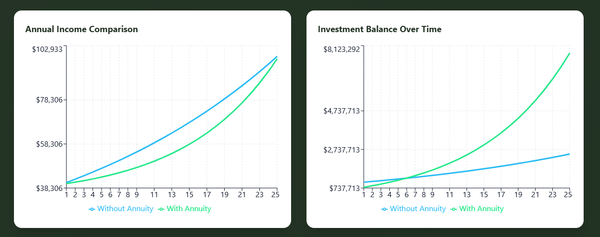

I read another “annuities are terrible” article today. The arguments were familiar: high fees, complexity, opportunity cost, and limited upside. And you know what? Some of that criticism is valid, but not for how I actually use Fixed Index Annuities (FIAs) with my clients. Here’s something important to establish

investment portfolio

The Gap Years Mistake

investment portfolio

Why perfectly reasonable assumptions break down in real retirement life

investment portfolio

If you’re 55-75 with retirement accounts, the OBBBA just raised your future tax bill. Not because of what it did to tax rates today. But because it increased tomorrow’s deficits. Deficits today mean tax hikes on visible wealth tomorrow. This is a matter of math, not politics. Subscribe

investment portfolio

We've covered a lot of ground in this series. You understand why pensioners have peace of mind that self-funded retirees often lack, and you know the mechanics of building your own Income Floor to bridge that gap. But knowing the strategy and actually implementing it are two different

Newsletter

In the first two parts of this series, we looked at why pensioners sleep better than self-funded retirees, even when they have less money in the bank. We explored the psychological weight of managing retirement income when every dollar depends on market performance, and we identified the real question you

retirement

Like most people, I’ve been watching the forecast this week. They’re calling for a big winter storm to move through our area beginning Saturday night, bringing a good amount of ice and snow. Maybe six inches. Maybe 18. Maybe it shifts slightly north, and we get rain. Subscribe

retirement

Previously, we looked at two types of retirees: the Pensioner and the Self-Funded Retiree. They show us that retirement income can be approached in very different ways, and that peace of mind isn’t just about the size of your savings. Today, I want to dig deeper into why pensioners

retirement

The two types of retirees

retirement

The woman sitting across from me had $1.8 million in her retirement accounts. She was 68 years old. Healthy. No debt. Pension coming in. Social Security started. Subscribe And she wouldn’t book the trip to see her grandkids. “I know I should go,” she told me during our