Why I Use Fixed Index Annuities (And Why Most Criticism Misses the Point)

I read another “annuities are terrible” article today. The arguments were familiar: high fees, complexity, opportunity cost, and limited upside. And you know what? Some of that criticism is valid, but not for how I actually use Fixed Index Annuities (FIAs) with my clients.

Here’s something important to establish up front: annuities are one financial tool that’s available to retirees. They’re the only tool I know of that can guarantee a lifetime income you cannot outlive. Like any tool, they’re useful in certain situations, but they’re not right for every job.

The problem with most annuity debates is that they treat all annuities as if they’re the same product serving the same purpose. They’re not. And more importantly, they completely miss the behavioral reality of retirement.

Let me be direct about how I think about FIAs, what they actually do, and when they make sense.

The Real Problem FIAs Solve (Hint: It’s Not Maximizing Returns)

Here’s what I’ve observed working with hundreds of pre-retirees: The clients with the most retirement anxiety aren’t necessarily the ones with the smallest portfolios. They’re often the ones lacking a guaranteed income floor. A report from Business Wire notes that 26% of retirees have lost sleep due to worries about their financial situation, showing how financial uncertainty can affect retirees’ well-being and the potential value of having a steady income in retirement.

Someone with a $500,000 portfolio and no pension loses sleep differently than someone with a $400,000 portfolio and a $30,000/year pension. The second person has peace of mind. The first person is running Monte Carlo simulations at 2am.

This is what I call The Pensioner’s Paradox. The retiree with guaranteed income covering their basic expenses often lives better psychologically and practically than someone with more assets but no income floor. This peace of mind can be attributed to the behavioral concept that ‘losses loom larger than gains,’ meaning the fear of losing financial stability outweighs the satisfaction of potential gains. Guaranteed income effectively diminishes this fear, allowing individuals to enjoy their retirement without the anxiety that accompanies volatile markets.

FIAs are not trying to beat the S&P 500. They’re trying to replicate what a pension does: provide a predictable income floor that you cannot outlive.

How I Actually Use FIAs (The Income-Growth Portfolio)

I don’t put 100% of someone’s money in an FIA. That would be insane.

I use what I call the Income-Growth Portfolio approach:

Income Floor (30-40% of portfolio): Fixed Index Annuities with guaranteed lifetime withdrawal benefits. For a $1 million portfolio, this means $300,000 to $400,000 is dedicated to covering essential expenses: housing, food, healthcare, and utilities. The stuff you need, regardless of what the market does.

Growth Engine (60-70% of portfolio): Invested for growth. This handles discretionary spending, travel, gifts to grandchildren, and legacy planning.

The FIA isn’t competing with your stock portfolio. It’s replacing the bond allocation that was supposed to provide “safety” but hasn’t kept up with inflation.

Here’s what this actually looks like in practice:

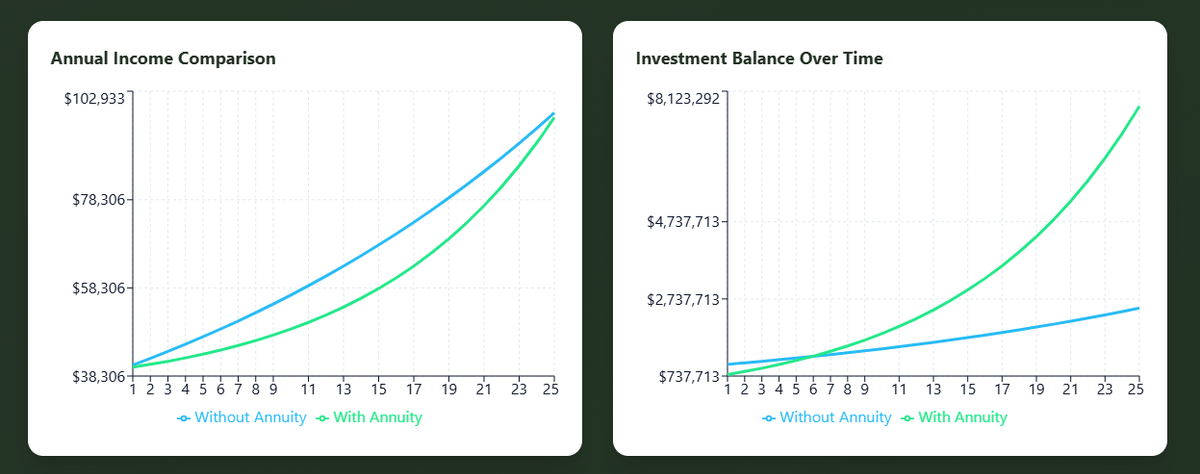

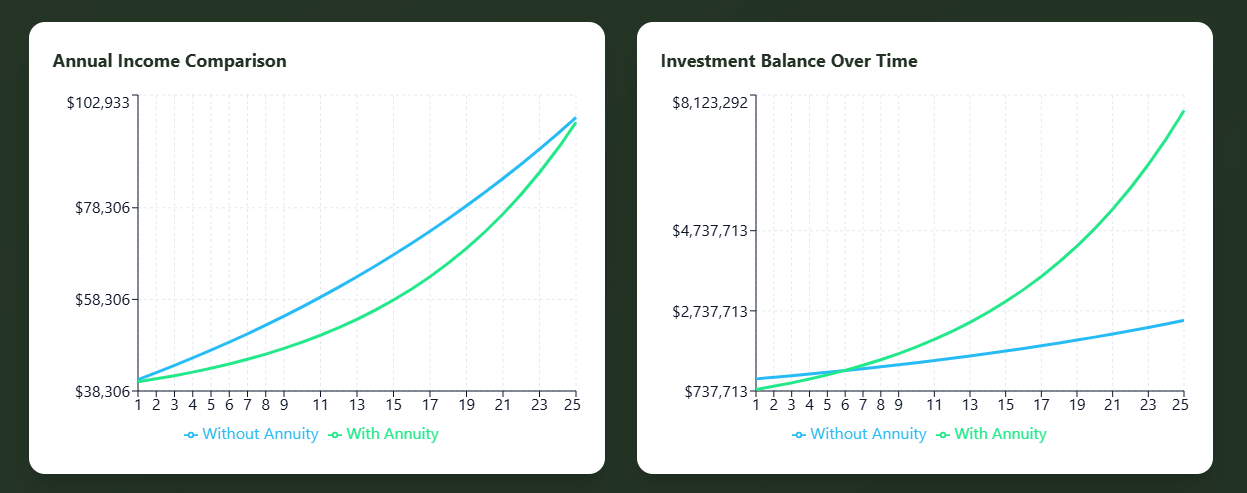

Let’s say you have $1 million at retirement. You allocate $300,000 (30%) to an FIA with a guaranteed lifetime withdrawal benefit that provides $34,000/year in income. The remaining $700,000 stays invested for growth.

[Insert charts showing Annual Income Comparison and Investment Balance Over Time]

Look at what happens over 25 years:

Annual Income: Both approaches provide similar income over time, but the Income-Growth Portfolio (green line) provides it with certainty. You know that $34,000 is guaranteed regardless of market performance.

Investment Balance: Here’s the surprising part: the portfolio WITH the annuity (green line) ends up significantly larger. Why? Because you’re not forced to sell investments at the worst possible times to generate income. The annuity provides your baseline spending needs, so your growth portfolio can actually stay invested and compound without being tapped for living expenses during market downturns.

This is the part that pure anti-annuity arguments miss: having guaranteed income can actually help you build MORE wealth, not less. When you know your essential expenses are covered, you can afford to leave your growth investments alone. You’re not panic-selling in bear markets to pay the mortgage. You’re not over-withdrawing from a declining portfolio and creating sequence-of-returns problems.

The Income-Growth Portfolio approach says: guarantee the essentials, let the rest actually grow. You end up with both more security AND more wealth.

The Honest Truth About FIA Downsides

Let me address the legitimate criticisms head-on:

Complexity: This is a fair point. FIAs are complex instruments. Let’s break down some of these terms: Cap rates are the maximum interest you can earn, similar to a speed limit on gains. Participation rates determine how much of the market gain is credited to your account, like sharing a percentage of a bonus. Spreads refer to the cost deducted from your gains, acting like a toll fee on your earnings. This is exactly why people need a CPA who understands these products in the context of their overall tax and retirement strategy, not someone who makes a commission and disappears.

Limited Upside: True. You’re not going to get 20% returns in an FIA. Instead, imagine it like paying an insurance premium to cap the storms: you trade the potential for high returns for certainty and protection. You won’t experience a -35% loss when the market crashes, which transforms the concept of a capped upside into a purposeful choice. The upside is carefully managed because the downside is completely eliminated.

Surrender Charges: Yes, FIAs typically have 5-10 year surrender periods. This is a problem if you might need 100% liquidity. It’s not a problem if you’re 65, have other liquid assets, and are building an income floor you won’t touch for 30 years.

Fees (on certain riders): Variable annuities can have fees of 2-3%. FIAs with income riders typically run 0.75-1.5%. (Finance, 2025) That’s the cost of the insurance guarantee. Is it worth it? Depends on what you value. Peace of mind isn’t free.

Here’s how the fees actually work: they’re calculated on the benefit base (the number used to determine your income), but they’re deducted from your account value. So yes, you’re paying fees that reduce your account balance. To make this more tangible, let’s consider an example. Suppose your FIA has a benefit base of $100,000 and an account value of $90,000. If there’s a 1% fee, $1,000 is calculated from the benefit base, but this amount is deducted from your account value, making it $89,000 after fees. Over time, this fee structure means your account balance decreases, but the guaranteed income remains based on the original benefit base.

But here’s the part that changes the equation: if you’re using an FIA correctly—as a lifetime guaranteed income stream—you’re going to deplete that account value to zero eventually anyway. The whole point is the income guarantee that continues even after your account hits zero.

In that context, the fees become less relevant. You’re not trying to maximize account value. You’re buying an income stream you can’t outlive. The fee is part of the cost of that guarantee.

The Legacy Question: Here’s a common misconception I need to address: “If I buy an annuity, the insurance company gets all my money when I die.”

That’s true if you annuitize—which means you exchange your lump sum for a guaranteed income stream and give up access to the principal.

But with an FIA that offers a guaranteed lifetime withdrawal benefit (GLWB), it works differently: if you die and there’s still money in the account, your beneficiaries get it. Every dollar that’s left goes to them, not the insurance company.

The insurance company only pays out from its reserves if you outlive your account balance. That’s the longevity insurance you’re buying. If you die at 72 with $200,000 still in the account, your kids get $200,000. If you live to 95 and the account hits zero at 87, the insurance company has been paying you for 8 years from their money, and your beneficiaries get nothing—but you got eight years of income you couldn’t have gotten anywhere else.

This is fundamentally different from traditional pension annuitization, where the insurance company keeps everything. With an FIA/GLWB structure, you maintain the possibility of legacy while getting the longevity protection.

What the Alternatives Actually Look Like

The common alternatives suggested are:

“Just invest in a diversified portfolio and use the 4% rule.” Great in theory. In practice, sequence-of-returns risk is real. If you retire into a bear market and start withdrawing 4%, you might not recover. Plus, the 4% rule assumes you’re comfortable watching your balance fluctuate by six figures year to year. Most people aren’t.

“Use dividend stocks for income.” Dividends get cut. Ask anyone who owned dividend stocks in 2008-2009. Or anyone who thought bank dividends were safe in perpetuity. Dividend income isn’t guaranteed.

“Build a bond ladder.” This can work well for creating a predictable income over a defined period. But it requires active management, rebalancing as bonds mature, and reinvestment decisions. At 65, that’s manageable. At 85, when you’re dealing with cognitive decline? Not so much.

“Sell covered calls or use options strategies for income.” These strategies can generate income in the right hands. But they require ongoing attention, market knowledge, and decision-making. They’re also strategies that can go wrong quickly if you’re not paying attention. Again—great at 65, potentially disastrous at 80.

“Just rely on Social Security.” For most of my clients, Social Security covers maybe 30-40% of their desired retirement spending. The gap between Social Security and actual expenses is exactly what we’re trying to solve.

“Buy bonds.” At recent interest rates, bonds are barely keeping up with inflation. And when rates rise, bond values fall. The whole point of bonds—capital preservation—has been challenged over the last few years (think 2022).

Here’s what most alternative strategies miss: retirement might last for 30 years, and you may not be sharp for all of them.

Bond ladders, dividend portfolio management, and options strategies all require ongoing decisions. What happens when you’re 82 and starting to show signs of cognitive decline? Who’s making those reinvestment decisions? Who’s monitoring the dividend portfolio? Who’s managing the options positions?

An FIA with a guaranteed lifetime withdrawal benefit requires zero ongoing decisions. You turn it on, the checks come every month for the rest of your life, regardless of your mental capacity. Your kids don’t have to take over managing investments. Your spouse doesn’t have to figure out what to do if something happens to you.

This “set it and forget it” aspect isn’t sexy. It doesn’t give you anything to optimize or manage. But at 85, that might be exactly what you need.

I’m not saying the other strategies are bad; many of them are perfectly fine for the right person. But they all assume you’ll remain capable of managing your finances indefinitely. An FIA doesn’t make that assumption.

When FIAs Make Sense (And When They Don’t)

Good fit:

- Age 55-75

- $500K-$2M in retirement assets

- Want guaranteed income covering basic expenses

- Have other liquid assets for emergencies

- Understand and accept limited upside in exchange for downside protection

- Value sleep-at-night factor

Bad fit:

Under 50 (too far from needing income)

Need 100% liquidity

Comfortable with portfolio volatility

Have a substantial pension already

The Tax Component

Here’s where being a CPA matters: FIAs can be incredibly powerful during the gap years between retirement and age 73 when RMDs kick in.

But not in the way most people think.

During ages 65-72, you have a unique tax planning opportunity. Your earned income has stopped, but your Required Minimum Distributions haven’t started yet. This is when smart retirees do aggressive Roth conversions—intentionally filling up the 22% or 24% tax brackets now to avoid being forced into higher brackets later when RMDs push up your taxable income.

Here’s where the Income-Growth Portfolio structure matters: you want to delay taking income from your annuity during these gap years if possible.

Why? Because every dollar of annuity income is a dollar of taxable income that fills up your lower brackets—brackets you want to use for Roth conversions instead.

The ideal scenario: Live off a combination of Roth withdrawals (tax-free), taxable account withdrawals (low capital gains rates), and strategic Roth conversions during ages 65-72. Keep the annuity income turned off if you don’t need it yet.

Then at 73, when RMDs start and your tax situation changes, you can turn on the annuity income if needed. Or keep it deferred even longer if your RMDs are manageable.

The benefit of having the FIA in place during the gap years isn’t that you’re taking income from it; it’s that you have the flexibility to take income from it if you need to, while you’re executing more valuable tax strategies with your qualified accounts.

This is advanced planning. It requires coordination among your retirement, income, tax, and investment strategies. It’s not something you get from buying an annuity from the first person who pitches you.

What I Tell Every Client Considering an FIA

This is not your entire portfolio. It’s one piece of a larger strategy.

You’re not buying this for returns. You’re buying it for psychological security and guaranteed income.

Understand the surrender period. If you might need this money in 5 years, don’t do it.

Know exactly what you’re paying. If your advisor can’t clearly explain the fees, find a different advisor.

This should integrate with your tax plan. An FIA without a tax strategy is half a solution.

Why the Way Annuities Are Typically Sold Creates Problems

Here’s something I need to address: much of the criticism you read about annuities isn’t really about the products themselves. It’s about how they’re sold.

And I’ll be honest—I understand the criticism.

The fear-based approach: I’ve seen too many presentations that lead with catastrophe. “The market is going to crash! You’ll lose everything! The only safe place for your money is right here!”

Look, markets are volatile. Sequence-of-returns risk is real. These are legitimate concerns. But using fear to push someone into a 10-year commitment without fully explaining the trade-offs isn’t financial planning—it’s just sales.

The oversimplification problem: “You get all the upside of the market with NONE of the downside! Plus guaranteed income for life! No risk whatsoever!”

This sounds great. It’s also not quite accurate. You don’t get “all the upside”—you get capped upside in exchange for downside protection. And there are risks—they’re just different risks. Liquidity risk. Inflation risk. Opportunity cost. Just because you can’t lose principal doesn’t mean there’s “no risk.”

What often gets left out: Too many clients have come to me with annuities they bought without fully understanding:

- Surrender charges that can last 10+ years

- The difference between “benefit base” (used to calculate income) and “account value” (what you actually have)

- Cap rates that can change annually

- How the income calculation actually works

- What happens to their money when they die

When I ask, “Did your advisor explain this?” the answer is usually “not really” or “he said not to worry about the details.”

That’s a problem. The details matter.

The commission structure most people don’t know about: Annuity commissions typically range from 4% to 8%, depending on the product. And here’s what creates misaligned incentives: higher commission products aren’t necessarily better for the client.

I’ve watched agents recommend 10-year surrender products over 5-year products because the commission is higher. I’ve seen riders added that boost the agent’s compensation, but that the client will likely never use.

This is exactly why I structure my practice differently. I charge separately for the Tax-Protected Income Blueprint planning work. If an annuity makes sense, that recommendation comes from comprehensive analysis—not from whatever product pays me the most.

WHen I recommend an FIA to a client, we address all of the factors I’ve listed in this article. My goal is for the client to fully understand the pros and cons of the specific product being considered. Here’s what the conversation should actually look like:

- What you’re giving up (liquidity, full market participation, flexibility)

- What you’re getting in return (guaranteed income floor, downside protection, longevity insurance)

- Why this specific product rather than the other options

- Exactly how the fees work and what I’m being paid

- The scenarios where you might regret this decision five years from now

- The alternatives we considered and why I think this makes more sense for your specific situation

If you’re not having that conversation with your advisor, you’re being sold a product rather than receiving advice. And that’s the real problem with annuities, not the products themselves, but the gap between what people need to know and what they’re actually told.

The Bottom Line

Are FIAs perfect? No. Are they right for everyone? Absolutely not. Do they serve a specific, valuable purpose for the right client? Yes.

The problem isn’t FIAs themselves. The problem is:

- Advisors using fear tactics instead of education

- Products being sold without full disclosure of downsides

- Commissions driving recommendations instead of client need

- People using them incorrectly

- Critics comparing them to investments when they’re insurance products

- Consumers expecting stock returns with zero risk

I use FIAs because I’ve seen what happens when retirees have no income floor. I’ve watched smart, successful people make terrible investment decisions in their 70s because they’re terrified of running out of money.

Having $800,000 fully invested is not better than having $500,000 invested and $300,000 providing $18,000/year in guaranteed lifetime income, at least not for most people I work with.

The real question isn’t “Are annuities good or bad?” It’s “Does this specific annuity, in this specific amount, for this specific purpose, make sense for this specific person?”

That’s a much harder question to answer. Which is exactly why you need someone who understands retirement tax planning, behavioral finance, and insurance products, not just someone trying to sell you something.

I help clients aged 55-75 with $500K-$2M in retirement savings design tax-efficient retirement income strategies. If you’re interested in learning whether the Income-Growth Portfolio approach makes sense for your situation, let’s talk.