The Pensioner Paradox: Part 2

Previously, we looked at two types of retirees: the Pensioner and the Self-Funded Retiree. They show us that retirement income can be approached in very different ways, and that peace of mind isn’t just about the size of your savings. Today, I want to dig deeper into why pensioners tend to sleep better at night. Understanding this can help you create a retirement plan that helps you rest easy, instead of worrying about the market.

The Emotional Math Doesn’t Add Up

This is where things get interesting, and where most financial advice often misses the mark.

Let me introduce you to two people. They’re the same age, have similar expenses, and live similar lifestyles. But their retirement experiences are very different.

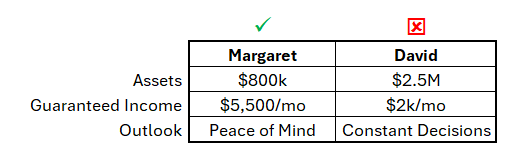

Scenario A: Margaret has $800,000 in her investment accounts. She also gets a $3,500 monthly pension from her years as a public school administrator and $2,000 from Social Security. Her guaranteed monthly income is $5,500. Every month. For life. No matter what the stock market does.

Scenario B: David has $2,500,000 in investments. That’s more than three times what Margaret has saved. He gets $2,000 from Social Security, but no pension. To cover his expenses, he needs to withdraw money from that $2.5 million portfolio every single month.

Now, here’s a question to consider: Which of these two people do you think sleeps better at night?

If you said Scenario A, you’re right. And if you said it immediately, without hesitation, you already understand something that most financial planning completely ignores.

Margaret always sleeps better, even though David has $1.7 million more in assets.

Why? Because certainty beats uncertainty, even when uncertainty comes with a much bigger number. Picture this: Margaret sips her morning coffee, a ritual as steady as the automatic deposit that lands in her account, unshaken by market fluctuations. It’s a simple moment, but one that sums up the peace of mind certainty brings.

This is the pensioner’s paradox. Margaret doesn’t have more money, but she does have more certainty. And that certainty is often worth more than we realize.

What “Keeping All the Risk” Actually Means

David didn’t choose to take on all the financial risk in retirement. He simply worked for companies that stopped offering pensions in the mid-1990s, so he ended up in this situation by default.

But the results of that default are very real.

Let’s look at what David manages every day. When I say he’s “keeping all the risk,” I don’t just mean market risk. He’s also carrying the mental and emotional weight of making sure his money lasts as long as he does.

Each year, David faces many decisions. Here’s what he has to handle:

He has to decide how much to withdraw. The 4% rule? Maybe 3.5% to be safe? Or can he go to 5% this year because the market did well? What if he withdraws too much and runs out of money at 85? What if he withdraws too little and dies at 78 with $3 million in the bank, having denied himself trips and experiences he could have afforded?

He has to rebalance during volatility. The market drops 20% in January. Does he sell bonds to buy stocks? Does he hold steady? Does he reduce his withdrawal rate this year to let the portfolio recover? Every decision has consequences he won’t know about for decades.

He has to manage taxes across multiple account types. Should he pull from the traditional IRA this year or the Roth? What about the taxable brokerage account? How much should he convert to Roth before his Required Minimum Distributions kick in? What’s his Medicare premium going to be in two years if he converts too much and crosses an IRMAA threshold?

He has to time Social Security. Start at 62? Wait until 70? What if he waits and dies at 68? What if he takes it early and lives to 95? What about his wife’s benefit? Spousal benefits? Survivor benefits?

And that’s only the technical side. He deals with this every year.

Then there’s the behavioral side, which can be even harder because it’s always on his mind, not just during yearly planning sessions.

There’s the risk of panic selling. If the market drops 30%, David’s withdrawal rate jumps from 4% to 5.7% overnight because his balance fell. Should he stay the course? He feels pressure to act.

There’s also analysis paralysis. With so many options and variables, David reads several articles about withdrawal strategies and ends up unsure whether to use a dynamic rule, a fixed percentage, or another approach. Too many choices leave him stuck.

There’s also the problem of underspending. David is so worried about running out of money that he lives more frugally than necessary. He skips vacations, doesn’t help his daughter with a down payment, and keeps driving his old car. In the end, he could pass away with a large balance, never having enjoyed the money he worked so hard to save.

There’s also the worry about living a long life. David wonders, what if he lives to 95, or his wife to 100? Should they downsize now to save money? What if healthcare costs rise sharply in their 80s?

Market anxiety is another issue. David checks his account balance daily, sometimes more than once. If the market drops 2%, he feels stressed. He hears news about corrections and wonders if he should move more money to bonds. He compares his returns to the S&P 500, even though that may not matter for his own plan.

Now, let’s go back to Margaret, the pensioner.

Margaret doesn’t deal with any of these issues.

It’s not because she has more money—she actually has less than a third of David’s assets.

Margaret doesn’t have to deal with David’s issues because the structure removed the burden. Structure beats uncertainty.

Her monthly income is $5,500. It arrives on the first of every month. It doesn’t matter if the stock market went up, down, or sideways. It doesn’t matter if we’re in a recession or a bull market. It doesn’t matter if inflation is running hot or cool, because her pension has a cost-of-living adjustment built in. If she lives to 95, that check still shows up. If her husband dies and she lives another 20 years, the survivor benefit keeps coming.

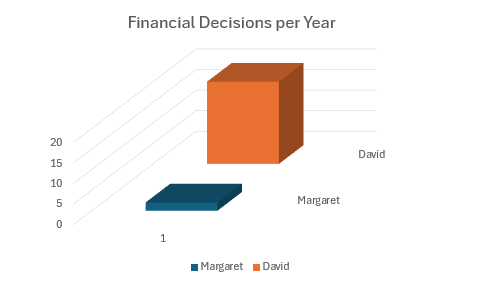

Margaret makes about two financial decisions per year: what to do with the extra money in her savings account and whether to take that trip to see the grandkids at Christmas or wait until spring.

That’s it. Those are her only major financial decisions.

They have similar retirements, but their mental experiences are completely different.

The Structural Advantage (Quantified)

Let me put some actual numbers to this psychological difference, because I think seeing it laid out makes the contrast even sharper.

Here’s what Margaret’s mental model of retirement looks like:

Her monthly income is $5,500, and it’s guaranteed. She doesn’t think about it as “withdrawing from a portfolio” or “managing a distribution strategy.” She thinks about it the same way she thought about her paycheck when she was working. It shows up. Every month. Forever.

Her inflation protection is built in. Her pension has a cost-of-living adjustment, so when prices go up, her income adjusts automatically. She doesn’t have to recalculate her withdrawal rate or worry about her purchasing power eroding over 30 years.

Her spouse protection is built in. If she dies first, her husband gets a survivor’s benefit. If he dies first, she keeps her full pension. This isn’t something she had to plan for or purchase separately. It’s just part of the structure.

Her longevity protection is built in. Whether she lives to 75 or 105, that income keeps coming. She can’t outlive it. This means she can spend confidently today without the nagging fear that she’s shortening her runway.

Her market exposure for income purposes is zero. The stock market can do whatever it wants. She has $800,000 invested, sure, and that money grows or shrinks with the market. But her day-to-day living expenses aren’t tied to those fluctuations. The market is something she reads about in the paper, not something that determines whether she can pay her electric bill.

Margaret only makes about two important financial decisions each year. Everything else runs automatically.

Now here’s David’s mental model:

His monthly income is variable. It depends on his portfolio balance, which depends on the market. He’s calculated that he can withdraw $8,300 per month using a 4% rule, and most of the time that works just fine. But when the market takes a dive, that $8,300 feels different coming out of a portfolio that’s down 15% than it does when things are humming along. The math says he’s fine, but the emotional experience shifts with every market swing.

His inflation protection is manual. If his costs go up, he needs to decide whether to increase his withdrawal rate or adjust his spending. There’s no automatic cost-of-living adjustment. It’s not complicated, exactly, but it does require him to make that call every year and live with the consequences.

His spouse’s protection is something he’s had to think through and plan for. Beneficiary designations, life insurance, and maybe some annuity options for his wife if he goes first. He’s got it handled, but it took work. It’s not built into the structure automatically. It’s something he had to engineer, with help from his advisor.

His longevity protection comes from planning and portfolio management. He’s run the projections. The Monte Carlo simulations look good. He’s probably fine. But “probably” isn’t quite the same as “guaranteed,” and he knows it. Most days, he doesn’t think about it, but when markets get choppy, or he reads another article about people living to 100, it crosses his mind.

His market exposure is significant because his income comes directly from his portfolio. If the market tanks the year after he retires, his sequence-of-returns risk is real. He understands this. His advisor has talked him through it. They’ve built in some buffers. But it’s there in the background, a variable he has to account for.

David has to make many more financial decisions than Margaret. He manages withdrawal rates, rebalancing, tax planning, Roth conversions, RMD strategies, and which account to use each month. While manageable with help, it takes ongoing attention and mental energy that Margaret doesn’t need to spend.

David’s mental workload isn’t impossible. Many people in his situation manage it. But it’s much higher than what Margaret faces, and for some, that difference matters more than the size of their account balance.

David has more money than Margaret. That’s objectively true. But Margaret has more built-in certainty. And for a lot of people approaching retirement, that certainty is worth more than the extra zeros in the account.

Why This Matters (The Aha Moment)

Most financial planning starts with the same question: “How much do I need to retire?”

You’ve probably asked it yourself. Maybe you’ve plugged numbers into one of those online calculators. Maybe you’ve had conversations with friends about whether $1.5 million is enough or if you really need $2 million to be safe.

I understand why you’d ask. It’s a common question, but it’s not the most important one.

Or at least, it should come second. The size of your portfolio only matters after you answer a more basic question first.

The right first question is: “How much guaranteed income do I need to cover my non-negotiable expenses?” To help you engage with this idea more practically, consider jotting down your essential expenses as a quick worksheet on the side. List items such as your rent, food, and medications. Capturing these details can turn your reading into a commitment toward understanding and planning for your financial needs.

Let me explain why looking at it this way makes such a big difference.

When you focus purely on asset size, you’re essentially asking: “How big does my pile of money need to be so that I can pull from it for 30 years without running out?” That’s a math problem. And it’s an important math problem. But it’s not actually the problem that keeps people up at night in retirement.

What keeps people up at night is uncertainty about whether they can pay their bills next month, next year, or ten years from now. It’s the fear of running out. It’s the anxiety about market timing. It’s the constant low-level stress of managing a portfolio that has to serve as both your paycheck and your safety net.

Once you know your guaranteed income number and have it covered, the question of asset size becomes less important. It’s still relevant, but it’s not the main focus.

Think about it this way. If you know with absolute certainty that $4,500 is going to show up every single month to cover your mortgage, your utilities, your food, your healthcare, and your basic transportation, then the question of whether you have $800,000 or $1.5 million in additional assets becomes a very different conversation.

That extra money is now for growth, discretionary spending, travel, helping your kids, or leaving a legacy. It’s no longer your survival fund. This shift in thinking makes a big psychological difference.

You can let that money ride out market ups and downs because you’re not relying on it for next month’s bills. You can invest more confidently, knowing your basic needs are covered, and make long-term decisions without fear.

This is what Margaret has that David doesn’t: a clear separation between the income she needs to live on and the assets she invests for growth.

Margaret’s $5,500 monthly pension and Social Security check cover her non-negotiables completely. Her $800,000 in investments? That’s gravy. It’s for the Alaska cruise. It’s for helping her granddaughter with college. It’s for upgrading the kitchen. She’s not stressed about that money because she doesn’t need it for survival.

David’s $2.5 million has to do both jobs at once. It has to generate his income and grow for the future, and serve as his safety net. That’s a lot to ask of a single pool of money, and it’s why his emotional experience of retirement is so different, despite having way more assets.

So when someone asks, “How much do I need to retire?” I always say, “Let’s first figure out how much guaranteed monthly income you need. Then we can talk about the assets required.”

The truth is, someone with $1 million and $4,000 a month in guaranteed income could be better off than someone with $2 million and no guaranteed income. It’s not just about net worth—it’s about real financial security and peace of mind.

The goal isn’t to have the biggest account balance. The real goal is to create a retirement plan that lets you sleep well, spend with confidence, and avoid worrying about every market change.

And that all starts with knowing your income floor number.

So here’s my question for you: Have you ever calculated your Income Floor number? Do you know how much guaranteed monthly income you actually need to cover your non-negotiables?

Drop a comment below with your biggest concern about retirement income. Is it market volatility? Running out of money? Managing all the decisions? I read every comment, and your answers will help me tailor the next post in this series.

Next week, I’m going to show you exactly how to build your own Income Floor using the Income-Growth Portfolio framework. Subscribe so you won’t miss it.