The Pensioner Paradox: Part 3

In the first two parts of this series, we looked at why pensioners sleep better than self-funded retirees, even when they have less money in the bank. We explored the psychological weight of managing retirement income when every dollar depends on market performance, and we identified the real question you should be asking: not "how much do I need to retire?" but "how much guaranteed income do I need to cover my non-negotiables?"

Today, we're rolling up our sleeves and getting practical. I'm going to walk you through the exact steps to build your own Income Floor using what I call the Income-Growth Portfolio framework. This is where theory meets reality, where you take control of your retirement structure instead of defaulting into anxiety. By the end of this post, you'll know precisely how to calculate your income gap, what tools are available to fill it, and how to position the rest of your portfolio for growth without the constant stress of wondering if you can afford to pay next month's bills. Let's get to work.

The Solution: Re-Creating the Pension Structure

Alright, here’s where we get practical. Because understanding the problem is one thing, but you’re reading this because you want to know what to actually do about it.

The goal here is straightforward: give self-funded investors the structural benefits of a pension without actually having one.

Let me be clear about what this is not. This is not about buying an annuity and calling it a day. Annuities are a tool, and sometimes they’re the right tool, but they’re not the strategy itself. This is not about abandoning growth or being overly conservative with your investments. And this is definitely not about eliminating all risk from your financial life, because that’s neither possible nor desirable.

What this is about is separating income from growth in your mind and in your portfolio structure. It’s about transferring specific risks—longevity risk, market timing risk, inflation risk—off your shoulders and onto institutions or instruments that are better equipped to handle them. And it’s about building decision-reducing systems so you’re not spending your retirement years making 20 financial decisions every time you sit down with your advisor.

The framework I’m going to walk you through is what I call the Income-Growth Portfolio. It’s designed to give you the peace of mind of a pensioner while preserving the upside and flexibility of a self-funded investor. And as a CPA, I’m going to show you how to layer in tax efficiency that most financial advisors completely overlook.

Let’s break this down step by step.

Step 1: Identify Your Income Floor Number

The Income Floor is the amount of monthly income you need to cover your non-negotiable expenses. These are the things you have to pay every single month, no matter what. The bills that don’t care if the market is up or down.

Non-negotiables include things like housing—your mortgage or rent, property taxes, homeowners’ insurance, HOA fees if you’ve got them. Utilities such as electricity, gas, water, and internet. Food, which means groceries and basic dining, not the fancy steakhouse, but the regular trips to the grocery store. Healthcare costs, such as insurance premiums and regular prescriptions. Transportation, whether that’s a car payment, insurance, gas, maintenance, or public transit passes if you’re in a city. And basic insurance coverage, like life insurance or any disability insurance, if you’re still working part-time.

What’s not included in your Income Floor? Travel. Entertainment. Gifts to family. Charitable giving. Discretionary shopping. The “nice to haves” that make life enjoyable but won’t result in a utility shutoff notice if you skip them for a month.

Let me give you a real example, because I think this is clearer with actual numbers.

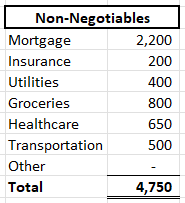

Meet Robert and Linda. Robert is 66, Linda is 64. They’re recently retired and trying to figure out if they’ve got enough to make this work. Here’s what their monthly non-negotiables look like:

Housing runs them $2,200 a month. That’s their mortgage payment, property taxes, and homeowners’ insurance rolled into one. Utilities are about $400—electric, gas, water, internet, the works. Food costs them around $800 a month for groceries and occasional basic meals out. Healthcare is $650, which covers their Medicare premiums, a supplement plan, and regular prescriptions for blood pressure and cholesterol meds. Transportation is $500—car insurance for two vehicles, gas, and setting aside money for maintenance and repairs. Basic insurance adds another $200 for a small life insurance policy that Robert still carries.

Add that all up, and Robert and Linda’s Income Floor need is $4,750 per month. That’s the number they need to hit every month, to keep the lights on and the mortgage paid. Everything else—the trip to visit their daughter in Colorado, the new furniture for the living room, helping their grandson with college—that’s all discretionary. Important, sure, but not part of the baseline survival number.

Your Income Floor number will be different. It might be higher if you live in an expensive area or have significant healthcare needs. It might be lower if your house is paid off or you’ve downsized. But the exercise is the same: add up everything you absolutely have to pay every month, and that’s your number.

Step 2: Calculate Your Guaranteed Income Sources

Once you know your Income Floor number, the next step is to figure out what you’ve already got in terms of guaranteed income. For most people, this starts with Social Security.

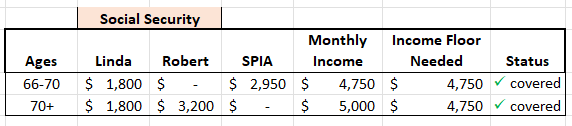

Robert and Linda’s situation looks like this. Robert is 66, and he’s decided to delay claiming his Social Security until age 70. By waiting, his benefit grows by about 8% per year, so instead of getting $2,400 a month at 66, he’ll get $3,200 a month at 70. Linda is 64 and plans to claim at her full retirement age of 67, which will give her $1,800 a month.

Neither of them has a pension. Robert worked in sales for a tech company that switched to a 401(k) plan back in the ‘90s. Linda worked part-time for years while raising their kids and then did administrative work for a small business that didn’t offer a pension either.

So, their current guaranteed income sources will be $ 5,000 per month once both of them are claiming Social Security at their optimal ages. Robert’s $3,200 plus Linda’s $1,800.

If you do have a pension, this is where you’d add it in. Some of you reading this might be in that fortunate position—maybe you worked for a school district, or a utility company, or you’ve got a union pension from years in a trade. If that’s you, add that monthly pension amount to your Social Security numbers and that’s your total guaranteed income.

Step 3: Identify the Gap

Now we’re getting to the heart of it. Robert and Linda need $4,750 a month to cover their Income Floor. Once they’re both claiming Social Security at their optimized ages, they’ll have $5,000 a month coming in. That’s actually a surplus of $250 a month, which sounds great.

But here’s the catch: Robert isn’t claiming until age 70. That’s four years away. And during those four years, their guaranteed income situation looks very different.

From ages 66 to 70, while Robert is delaying his benefit, they’ve only got Linda’s $1,800 per month from Social Security. Their Income Floor need is still $4,750. That means they’ve got a $ 2,950-per-month gap that needs to be filled for 4 years.

This is a critical point that many retirement plans miss. It’s not enough to know that your Social Security will eventually cover your needs. You have to figure out how you’re going to bridge the gap during those in-between years, especially if you’re delaying benefits to maximize your monthly check later.

If Robert and Linda don’t have a plan for that $2,950 monthly gap, they’ll be forced to withdraw from their investment portfolio when the market might not cooperate. And if the market happens to tank in year one of their retirement—which, let’s be honest, is exactly when sequence-of-returns risk is most dangerous—they could be locking in losses and permanently damaging their long-term financial security.

So the gap isn’t just a number on a spreadsheet. It’s a real vulnerability in their retirement plan that needs to be addressed with intention, not just by hoping the market behaves itself for the first four years.

Step 4: Fill the Gap (The Pension Recreation)

This is where we actually build the pension-like structure that will give Robert and Linda the peace of mind we’ve been talking about. There are several ways to fill an Income Floor gap, and the right choice depends on your specific situation, your comfort level with different financial tools, and frankly, how much flexibility you want to preserve.

Let me walk you through the main options.

Option A: Use Guaranteed Income Tools

The most direct way to fill the gap is with an income annuity. Now, I know what some of you are thinking. “Annuities? Aren’t those the things with the high fees that lock up my money forever?” And yes, some annuities are terrible products with high costs and surrender charges that would make a loan shark blush. But a simple, single-premium immediate annuity—often called a SPIA—is actually a pretty straightforward tool for creating guaranteed income.

Here’s how this would work for Robert and Linda. They withdraw $200,000 from their investment portfolio and purchase a SPIA that pays them $2,950 per month for a specific period—in this case, 4 years, the gap between now and when Robert claims Social Security at 70. This is called a “period certain” annuity, which just means it pays for a set number of years rather than for life.

The result? From ages 66 to 70, they’ve got $1,800 from Linda’s Social Security and $2,950 from the annuity, which adds up to their $4,750 Income Floor. Check. Then, at age 70, Robert’s Social Security kicks in at $3,200, Linda’s continues at $1,800, and the annuity payments stop because they’re no longer needed. Now they’ve got $5,000 in guaranteed monthly income. That’s actually $250 more than their Income Floor need, which gives them a little breathing room or some extra money for discretionary spending.

The beauty of this approach is that Robert and Linda’s basic living expenses are now fully covered for life, without them having to touch their investment portfolio for day-to-day expenses. The cognitive load drops dramatically because they’re not making monthly decisions about how much to withdraw or whether the market can support their spending this year.

Another variation on this is a deferred income annuity, or DIA, which you can think of as buying a future pension. Let’s say Robert and Linda are worried not just about the next four years, but also about what happens when they’re 80 or 85, potentially facing higher healthcare costs. They could use part of that $200,000 to purchase a DIA that starts paying them additional income at age 80. It’s pension-like income on a delayed basis, providing a safety net for those later years when cognitive decline might make financial management harder.

Option B: Create a Bond Ladder

If the idea of handing $200,000 to an insurance company makes you uncomfortable—and I get it, it’s not a small amount of money—you can create your own income stream using a bond ladder or a CD ladder.

Here’s how this works. Robert and Linda would set aside $150,000 in short-term, high-quality bonds or CDs, structured so that roughly $2,950 matures each month for the next 4 years. This gives them the income they need to fill the gap, and they retain more control and flexibility than they would with an annuity.

The downside? It requires more management. Bonds mature; you have to reinvest or spend down; you’re monitoring interest rates; and you’re taking on the responsibility of making sure the ladder is structured correctly. It’s not overly complicated, but it does add to that cognitive load we’ve been trying to reduce.

The upside? You preserve flexibility. If something unexpected happens—a medical emergency, a need to access that capital for some other reason—the money is yours, and you can get to it. With an annuity, once you’ve purchased it, that money is generally locked in.

Option C: Combination Approach

This is often the sweet spot for many people, and it’s what I tend to recommend when someone wants both security and flexibility. You use part of the money for bonds or CDs to cover the first couple of years, and then you layer in an annuity or DIA to cover the later years or to provide lifetime income beyond Social Security.

For example, Robert and Linda could set aside $100,000 in a two-year bond ladder to cover the first two years of the gap. That gives them $2,950 a month from bonds while they ease into retirement, see how their spending actually shakes out in real life versus what they projected on paper, and get comfortable with the whole process. Then they use another $100,000 to purchase a deferred income annuity that starts paying at age 68, which bridges them to Robert’s Social Security starting at 70.

This approach gives them immediate flexibility and control for the first two years, guaranteed income for the next two, and then full Social Security coverage from 70 onward. It’s a blend of control and certainty, and for many people, that feels better than going all-in on one approach or the other.

Step 5: Invest the Rest for Growth

Now here’s where things get really interesting, because once you’ve handled the Income Floor, everything else in your portfolio has a completely different job.

Robert and Linda started with $1,500,000 in total investments. They used $200,000 to purchase the SPIA that fills their income gap for four years. That leaves them with $1,300,000 in what I call the Growth Portfolio.

And here’s the key: this $1,300,000 is no longer responsible for generating their day-to-day income. It’s not their paycheck. It’s not the money that keeps the lights on. It’s invested for long-term growth, discretionary spending, legacy, unexpected expenses, and to give them options down the road.

This psychological separation is everything. Because now, when the market drops 15%, Robert isn’t lying awake at night wondering if he can still afford to pay the mortgage. His mortgage is covered by his Income Floor. The Growth Portfolio can be down 15%, or 20%, or even 30% in a really bad year, and his basic standard of living doesn’t change at all.

That means Robert and Linda can invest this Growth Portfolio more aggressively than they ever could if it were also serving as their income source. They can ride out volatility without panic. They can rebalance annually instead of constantly tinkering. They can make rational, long-term decisions instead of emotional, fear-based ones.

Here’s how I’d typically structure their Growth Portfolio: 70% in stocks and 30% in bonds. That’s more aggressive than most 66-year-olds would be comfortable with if their entire retirement income depended on that portfolio. But Robert and Linda’s income doesn’t depend on it. Their Income Floor is secure. So they can afford to take on more equity exposure and capture more long-term growth.

They rebalance once a year, usually in January. They harvest tax losses when it makes sense. And they optimize withdrawals for tax efficiency, which is where having a CPA in your corner really starts to pay off, because we’re going to use those gap years before Robert’s Social Security starts to do some Roth conversions that will save them tens of thousands of dollars in taxes over their lifetime. But I’m getting ahead of myself. We’ll come back to the tax piece in a minute.

The point is this: the Growth Portfolio has one job, and that job is growth. It’s not trying to be their paycheck, their safety net, and their legacy fund all at once. It’s just trying to grow steadily and intelligently, over a long time horizon. And because it has that singular focus, it can do that job really well.

Now it’s your turn. Take 10 minutes this week and do this exercise:

- Calculate your monthly non-negotiables

- Add up your guaranteed income sources (Social Security, pension if you have one)

- Identify your gap

Reply to this email or comment below with what you found. Do you have a gap? How big is it? I’ll respond to every comment and let you know if you’re on the right track.

In the final post of this series, I’m going to show you the psychological transformation that happens when you implement this framework, plus the tax optimization layer that most financial advisors completely miss. That’s where the real money gets saved.

See you next time.

If you subscribe to my Substack, you’ll get a free, downloadable version of my Tax-Protected Retirement Income Audit worksheet in your welcome email.