The Pensioner Paradox: Part 4 (final)

We've covered a lot of ground in this series. You understand why pensioners have peace of mind that self-funded retirees often lack, and you know the mechanics of building your own Income Floor to bridge that gap. But knowing the strategy and actually implementing it are two different things, and that's what I want to address today.

What does it actually feel like when you shift from worrying about your portfolio balance every time the market dips to having genuine confidence that your bills are covered no matter what? How much money can you actually save over a 30-year retirement by being strategic about taxes during those critical gap years before Social Security kicks in? And what does the complete Income-Growth Portfolio framework look like when you put all the pieces together?

This is where we bring it home. This is where the structure you've built transforms from a plan on paper into the peace of mind you've been working toward your entire career. Let's finish this.

The Psychological Transformation

Let me show you what this looks like in practice, because the difference between “before” and “after” implementing an Income-Growth Portfolio structure is dramatic.

Before they set up their Income Floor, here’s what Robert’s daily life looked like. He’s checking his portfolio balance on his phone. Not obsessively, but regularly. Maybe once in the morning with his coffee, maybe again in the evening while he’s watching the news. The market drops 15% over a couple of weeks—which happens, markets do this—and Robert feels it in his chest. He’s doing the math in his head. If his $1.5 million portfolio is now $1.275 million, and he’s planning to withdraw 4% annually, that’s... wait, that’s less than he was counting on. Should they cut their spending? Should they cancel the trip they were planning to take to visit their son in Seattle? He’s not sure. He doesn’t know if they can afford it anymore. The number on the screen has changed, so everything feels uncertain.

Robert calls his financial advisor. They have a conversation. The advisor assures him that this is normal volatility, that the plan is still sound, and that they built in buffers for exactly this scenario. Robert feels better for a day or two. Then the market drops another 3%, and he’s back to checking his balance and wondering if they should be doing something different.

It’s not that Robert is irrational or overly anxious. He’s just trying to manage a complex system in which every variable affects every other, and the primary variable—the market—is completely outside his control. His retirement security and the stock market are coupled together, and when one moves, he feels it directly.

Now here’s Robert after they’ve implemented the Income-Growth Portfolio structure.

The market drops 15%. Robert sees it on the news. He might even check his account balance, because old habits die hard. And yes, his Growth Portfolio is down from $1.3 million to somewhere around $1.1 million. That’s real money. That’s not nothing.

But here’s the difference: Robert knows that his $4,750 in monthly expenses is covered. Completely covered. Linda’s Social Security check is coming. The annuity payment is coming. Those don’t care what the market did today, this week, or this month. His mortgage gets paid. The electric bill gets paid. The prescriptions get refilled. None of that is in question.

So when Robert looks at that $1.1 million balance, he doesn’t panic. He shrugs. “The market’s down. It’ll come back eventually. Our bills are covered. The growth portfolio is for the long term. We’ll ride it out.”

And then he goes about his day. Maybe he and Linda still take that trip to Seattle, since it isn’t coming out of the Growth Portfolio anyway. It’s coming out of the surplus they’ve built up over the last year from that extra $250 a month their Social Security provides above their Income Floor need.

Same assets. Same market drop. Completely different emotional experience.

That’s the power of structure. Robert didn’t get calmer because he had more money. He got calmer because his basic needs are decoupled from market volatility. The Income Floor has created a psychological safety net that allows him to be a rational investor with the rest of his portfolio, rather than a scared retiree trying to make sure he doesn’t run out of money.

And here’s the other side of this that’s equally important: Robert can now spend confidently from his guaranteed income without guilt or fear. Many retirees, especially self-funded ones, suffer from what I call “spending paralysis.” They’ve saved diligently for 40 years. They’ve accumulated a substantial nest egg. And then they get to retirement and can’t bring themselves to spend the money because they’re terrified of running out.

Robert and Linda don’t have that problem anymore. Their Income Floor of $4,750 is guaranteed for life. That money is meant to be spent. It’s their paycheck. They’re not depleting an asset when they spend it. They’re just using their income, the same way they did when Robert was working. The psychological permission that creates is huge.

Meanwhile, the Growth Portfolio becomes “legacy and bonus money” in their minds. It’s there for the big discretionary purchases, for helping their kids if needed, for leaving something behind. But it’s not their survival fund. It can fluctuate without triggering that primal fear response that comes from feeling like your basic security is at risk.

This mental separation—income over here, growth over there—gives Robert’s brain permission to do two things simultaneously that feel contradictory but aren’t. He can spend confidently from his guaranteed income because it’s designed to be spent and won’t run out. And he can ignore volatility in his growth portfolio because he doesn’t need that money for survival, so short-term fluctuations are just noise.

The structure creates the emotional space for rational decision-making. And that, more than any investment return or tax strategy, is what allows people to actually enjoy their retirement instead of spending it anxiously monitoring account balances and second-guessing every spending decision.

The Tax Layer

Alright, here’s where most financial advisors stop, and where a CPA with a tax-planning mindset starts adding real value.

The average advisor will help you figure out your Income Floor number, maybe recommend an annuity to fill the gap, and call it a day. “You need $4,750 a month in guaranteed income. Here’s a SPIA that provides it. Problem solved.”

And look, that’s not wrong. But it’s incomplete. Because here’s the question nobody’s asking: where is that income coming from, tax-wise, and can we structure it more efficiently?

This is where the real money gets saved over a 30-year retirement. We’re not talking about finding a few extra deductions on your tax return. We’re talking about potentially six figures in tax savings over your lifetime by being strategic about which accounts you pull from, when you take income, and how you layer in Roth conversions during those critical gap years.

Let me show you what this looks like for Robert and Linda, because the tax opportunities in their situation are substantial.

Remember, Robert is delaying Social Security until age 70, creating a 4-year gap from ages 66 to 70. Most people see this gap as a problem to be solved—how do we generate income during these years? But a CPA sees it as an opportunity. Because Robert and Linda’s taxable income during those four years will be unusually low, low-income years are golden opportunities for Roth conversions.

Here’s their tax situation during the gap years. Linda’s Social Security is $1,800 a month, which is $21,600 annually. Depending on their other income, between 0% and 85% of it will be taxable. Let’s assume they’re at the middle ground, with about 50% of Social Security taxable, so that’s roughly $11,000 in taxable income from Social Security.

The annuity payment of $2,950 per month is $35,400 annually. But here’s the thing about annuity income: part of it is considered a return of your principal, and part is considered earnings. The principal portion isn’t taxable. You already paid tax on that money when you earned it years ago. Only the earnings portion is taxable. In a typical SPIA structure, maybe 30-40% of each payment is taxable in the early years. So let’s say $12,000 of that $35,400 is taxable income.

Add it up, and Robert and Linda have roughly $23,000 in taxable income during these gap years. That’s it. They’re nowhere near the top of the 12% tax bracket, which for a married couple filing jointly is about $94,000 in taxable income.

So here’s what we do: we convert traditional IRA money to Roth, and we convert enough to fill up the rest of that 12% bracket without pushing them into the 22% bracket. That means we can convert roughly $70,000 per year from Robert’s traditional IRA to a Roth IRA and pay tax at just 12% on that conversion.

Now, you might be thinking, “Wait, why would I voluntarily pay tax on $70,000 if I don’t have to?” Great question. Here’s why: Robert is 66. His Required Minimum Distributions don’t start until age 73, giving him 7 years of conversion opportunity. If he waits and does nothing, here’s what happens. His traditional IRA—let’s say he has $800,000 in it—continues to grow. By the time he’s 73, it might be worth $1.1 million or more. Now the IRS says he has to start taking RMDs, which are calculated as a percentage of the account balance.

At age 73, that percentage is roughly 3.8%, so his first RMD would be around $42,000. But remember, by age 73, Robert is also collecting $3,200 a month in Social Security. That’s $38,400 annually. Linda’s collecting $1,800, which is $21,600 annually. Their Social Security alone is $60,000. Now add the $42,000 RMD on top of that, and they’ve got $102,000 in taxable income, which pushes them well into the 22% tax bracket.

And it gets worse. Those RMDs increase every year as a percentage of the remaining balance, and if Robert passes away first, Linda becomes a single filer with a much smaller standard deduction and narrower tax brackets. That $42,000 RMD that was taxed at 22% in their joint return might now be taxed at 24% or even 32% on Linda’s single return.

Oh, and let’s not forget about Medicare IRMAA surcharges. If Robert and Linda’s modified adjusted gross income exceeds certain thresholds—currently around $206,000 for a married couple—they start paying extra for Medicare Part B and Part D. Those surcharges can add hundreds of dollars per month to their healthcare costs. Unnecessary, avoidable costs that come directly from poor tax planning.

So here’s the alternative. During those four gap years from ages 66 to 70, we convert $70,000 per year from a traditional IRA to a Roth. That’s $280,000 total converted at a 12% tax rate. Yes, they’re paying about $33,600 in taxes over those four years. But that $280,000 is now in a Roth IRA where it will never be taxed again. Not when it grows. Not when they withdraw it. Not when Linda inherits it after Robert dies. Never.

Fast forward to age 73. Instead of having $1.1 million in his traditional IRA generating a $42,000 RMD, Robert now has maybe $650,000 in his traditional IRA, and his RMD is only about $25,000. His taxable income is Social Security plus a much smaller RMD, which keeps him in the 12% bracket instead of the 22% bracket. And if he passes away first, Linda’s tax situation as a single filer is far more manageable, since she inherited a large Roth IRA that doesn’t require taxable RMDs.

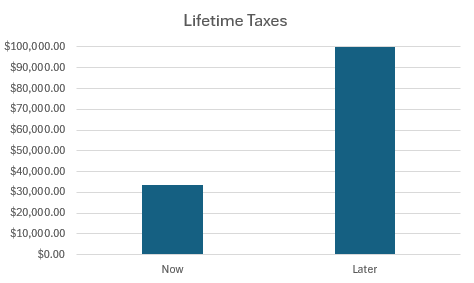

Over a 30-year retirement, the tax savings from this strategy can easily exceed $100,000. We paid $33,600 in tax during the gap years to save multiples of that amount over the rest of their lives. That’s the power of proactive tax planning.

What’s the better deal: Pay $33k now or $100k later? Good retirement planning minimizes tax over your lifetime, not just this year. Smart moves, such as timely Roth conversions during gap years, can help lower your lifetime tax bill substantially. By choosing to convert during the 12% bracket years, we’re opting to pay around $33,600 in taxes today to save potentially over $100,000 in future taxes during retirement.

And here’s the other benefit that doesn’t show up on a spreadsheet: flexibility. That Roth IRA gives Robert and Linda options. If they need a large chunk of money for an unexpected expense—a new roof, a medical procedure, helping a child through a financial crisis—they can pull from the Roth without triggering a massive tax bill or pushing themselves into IRMAA surcharge territory. The Roth is a tax-free emergency fund that also grows.

Now, let’s also talk about the tax efficiency of their ongoing Income Floor once Robert starts collecting Social Security at age 70. Their $5,000 monthly Social Security income is taxed favorably. Even if 85% of it is taxable—the maximum—that’s only $51,000 in taxable Social Security income. Add in a modest RMD from what’s left in the traditional IRA, and they’re still comfortably in the 12% bracket with room to spare.

Meanwhile, their Growth Portfolio is structured for tax efficiency as well. We’re holding tax-inefficient investments, such as bonds and REITs, in their traditional IRAs. We’re holding tax-efficient investments, such as index funds and municipal bonds, in their taxable brokerage account. We’re doing tax-loss harvesting when opportunities arise. We’re being smart about which account we pull from for discretionary spending.

This is the tax layer that most retirement planning completely ignores. And it’s the layer where a good CPA saves you more money than you’ll ever pay in planning fees.

Most financial advisors can tell you to buy an annuity. That’s fine. But can they tell you how to structure your income sources to minimize lifetime tax liability while also avoiding Medicare surcharges and setting up your spouse for success if you die first? That’s a different conversation entirely.

And that’s the conversation you should be having.

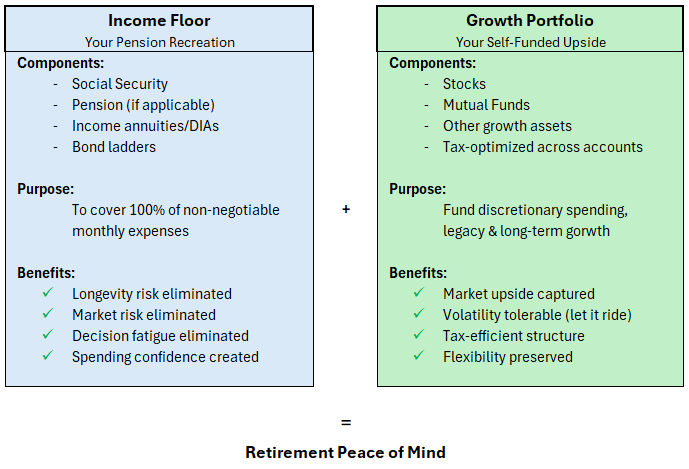

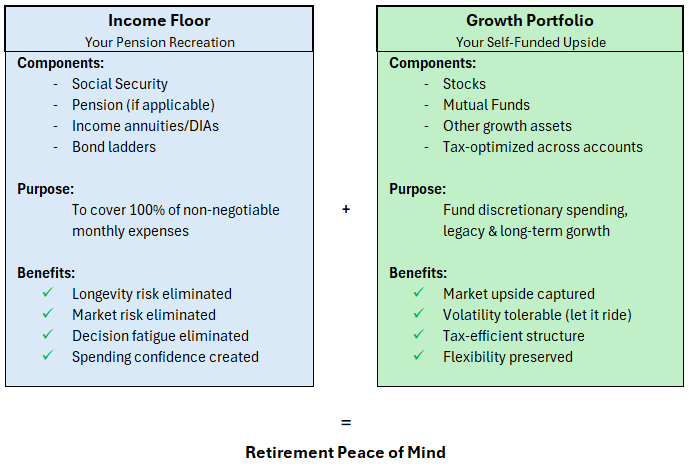

The Income-Growth Portfolio: Final Framework

Let me pull all of this together into a clear framework you can actually use, because I don’t want you walking away from this with just a bunch of theory. I want you to have a mental model you can apply to your own situation.

The Income-Growth Portfolio has two distinct components, and keeping them separate in your mind is the key to making this whole thing work.

First, you’ve got your Income Floor. This is your pensioner-like structure. It’s built on Social Security and optimized with the right claiming strategy for your situation. If you’re fortunate enough to have a pension, that goes here too. And then you fill whatever gap exists using income annuities, deferred income annuities, bond ladders, or some combination of those tools, depending on your preference for guaranteed income versus flexibility.

The goal of the Income Floor is simple: cover 100% of your non-negotiable monthly expenses with income sources that aren’t dependent on the stock market. This is your rent money, your grocery money, your utility money, your healthcare money. The stuff that has to get paid, no matter what the Dow Jones did today.

The psychological benefit of the Income Floor is that you’ve transferred longevity risk and market timing risk off your shoulders. You can’t outlive this income. It doesn’t matter if you make it to 95 or 105. The checks keep coming. And it doesn’t matter if the market crashes the year after you retire. Your bills are covered.

Second, you’ve got your Growth Portfolio. This is your self-funded upside. It’s market-based, invested for long-term growth, and tax-optimized through strategies like Roth conversions, tax-loss harvesting, and smart withdrawal sequencing.

The goal of the Growth Portfolio is to grow over time so you can cover discretionary spending, fund your travel and hobbies, help your kids or grandkids if you want to, and leave a legacy. But critically, this money is not needed for your day-to-day survival. You’re not withdrawing from it every month to pay the mortgage. You’re letting it grow and using it strategically to make retirement enjoyable rather than just survivable.

The psychological benefit of the Growth Portfolio is that you can tolerate market volatility without panic. Your Income Floor has removed the existential fear of running out of money, which means your Growth Portfolio can actually do its job—grow—without you sabotaging it by selling at the bottom of every correction because you’re scared.

When you put these two components together, here’s what you get: the security of a pensioner combined with the upside of a self-funded investor, all wrapped in the tax efficiency of a CPA-designed plan.

You’ve got guaranteed income covering your basics. You’ve got growth potential for everything else. And you’ve got a tax strategy that keeps more of your money in your pocket instead of sending it to the IRS unnecessarily.

That’s the framework. Income Floor plus Growth Portfolio equals a retirement you can actually enjoy instead of spending it worried about whether you’ve got enough.

You Can’t Turn Back Time, But You Can Build Certainty

Here’s the truth, and I’m not going to sugarcoat it: traditional pensions are gone for most people. If you’re reading this and you’re under 60, the odds that you’ve got a defined benefit pension waiting for you at retirement are slim. And if you’re over 60 and you don’t have one by now, you’re not getting one. The corporate world moved away from pensions decades ago, and that ship has sailed.

You can’t turn back the clock to 1985, when companies were still offering those defined benefit plans that guaranteed you a paycheck for life. That world no longer exists for the vast majority of workers.

But here’s the thing: you can engineer the same outcome. The pension wasn’t magic. It was just a system, a structure that provided specific benefits. It gave you guaranteed monthly income. It removed longevity risk by paying you for as long as you lived. It removed market timing risk by decoupling your income from stock market volatility. And it reduced decision fatigue by putting your retirement income on autopilot.

Every single one of those benefits is replicable. You can build all four of those features using the tools we’ve talked about: Social Security optimization, income annuities, bond ladders, tax planning, and intelligent portfolio structure.

The structure is replicable. The peace of mind is achievable. You just need a plan that prioritizes income certainty over maximizing account balance.

And that’s the shift I want you to make mentally as you think about your own retirement. Stop asking yourself, “Do I have enough in my accounts?” and start asking, “Do I have enough guaranteed income to cover my non-negotiables?”

Once you’ve answered that second question, the first question becomes a lot less scary. Because the truth is, you might need less in total assets than you think if you’ve structured your income properly. Or you might discover you need more, but now you’ve got time to adjust and plan instead of just hoping the 4% rule works out in your favor.

The Income-Growth Portfolio framework gives you a roadmap. It shows you exactly what you need to build, why you need to build it, and how the pieces fit together to create both security and growth.

Margaret, our pensioner from the beginning of this piece, didn’t do anything special to earn her peace of mind. She just happened to work for an employer that offered a pension. That structural advantage was handed to her. David, our self-funded investor, didn’t do anything wrong. He worked hard, he saved diligently, and he accumulated $2.5 million. But the structure he defaulted into—no pension, all assets, all risk—creates a fundamentally different emotional experience of retirement.

You can close that gap. You can give yourself the structural advantages that Margaret has, even if you don’t have a pension. It takes intentionality. It takes planning. And yes, it takes working with people who understand both the financial tools and the tax implications.

But it’s doable. And the payoff isn’t just financial. It’s psychological. It’s the ability to sleep at night. It’s the freedom to spend confidently without guilt or fear. It’s the peace of mind that comes from knowing your basics are covered, no matter what the market does.

That’s what the Income-Growth Portfolio is designed to deliver. Not the biggest possible account balance. Not the highest investment returns. Not the most complex financial plan.

Just a retirement where you can breathe easy, enjoy your life, and not check your portfolio balance every time the market has a bad day.

And honestly, isn’t that what you’ve been working toward all along?

Let’s Make This Real

Here’s what I want you to do next, because reading about this framework is one thing, but applying it to your own situation is where the value actually shows up.

Sit down and calculate your Income Floor number. Add up everything you absolutely have to pay every month. Housing, utilities, food, healthcare, transportation, insurance. Write down the total. That’s your number.

Then figure out what you’ve already got in guaranteed income. Social Security for you and your spouse, optimized for the right claiming ages. Pension if you’ve got one. Add those up.

If there’s a gap between what you need and what you’ve got guaranteed, you’ve just identified the problem you need to solve. And now you know the tools available to solve it: annuities, bond ladders, Roth conversions during low-income years, tax-optimized withdrawal strategies.

If you want to talk through your specific situation, reply to this post or send me a message with your monthly non-negotiables and your current guaranteed income sources. I’ll tell you if you’ve got a gap, how big it is, and what your options look like for filling it.

Because here’s the thing: this isn’t theoretical. This is your retirement. And you deserve to enjoy it instead of spending it anxious about whether you’ve saved enough.

Let’s build you some certainty.

P.S. If this series helped you think differently about retirement planning, would you share it with a friend who’s approaching retirement? The peace of mind this framework creates is too valuable to keep to yourself. Thanks.