The Problem With the 4% Rule Isn't the Math

Why perfectly reasonable assumptions break down in real retirement life

The 4% rule is one of the most widely cited pieces of retirement planning advice. It’s well-researched, tested against historical data, and mathematically defensible. People love it because it does something rare in financial planning: it gives a clear, simple answer to an emotional question. “How much can I safely withdraw from my portfolio each year without running out of money?” Four percent. Done.

The rule isn’t foolish. It’s logical. And that’s why it’s so persuasive. It takes something terrifying: the possibility of running out of money, and turns it into a number you can calculate on a napkin. But here’s what I’ve learned after building retirement plans for hundreds of clients: the 4% rule doesn’t fail because the math is wrong. It struggles because the assumptions underneath it are more fragile than most people realize.

Let’s start with what the 4% rule actually assumes. The rule assumes markets behave roughly in line with historical averages over your retirement. It assumes you withdraw money mechanically, adjusting only for inflation, regardless of what’s happening around you. It assumes you stay disciplined through volatility: you don’t panic in 2008, you don’t second-guess yourself in 2020, and you don’t adjust when headlines scream crisis. It assumes taxes are stable or secondary. And it assumes your life unfolds neatly over a predictable 30-year window.

None of these assumptions is crazy. But they’re not guaranteed. And when even one breaks down, the entire structure shifts. The rule doesn’t fail due to a mathematical error. It struggles because real retirement doesn’t operate in the clean, frictionless environment the math requires.

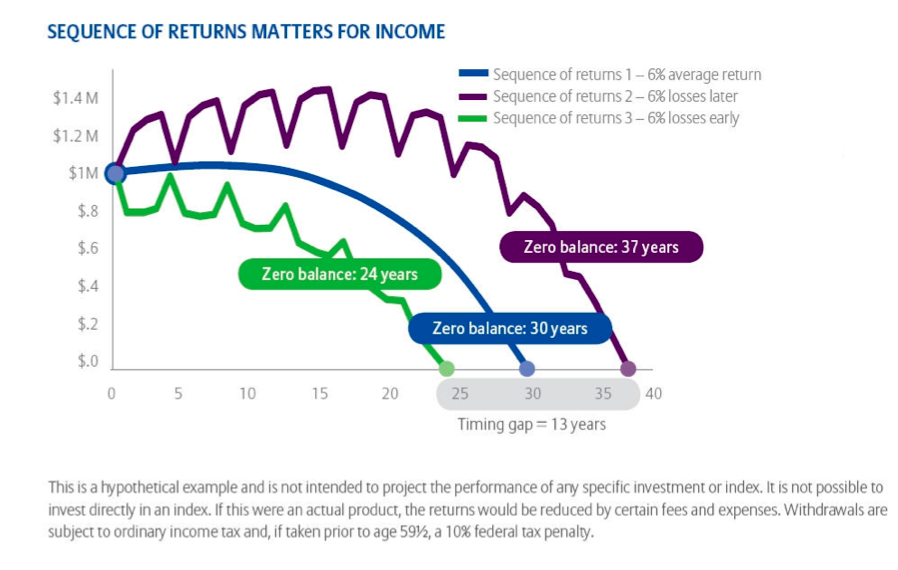

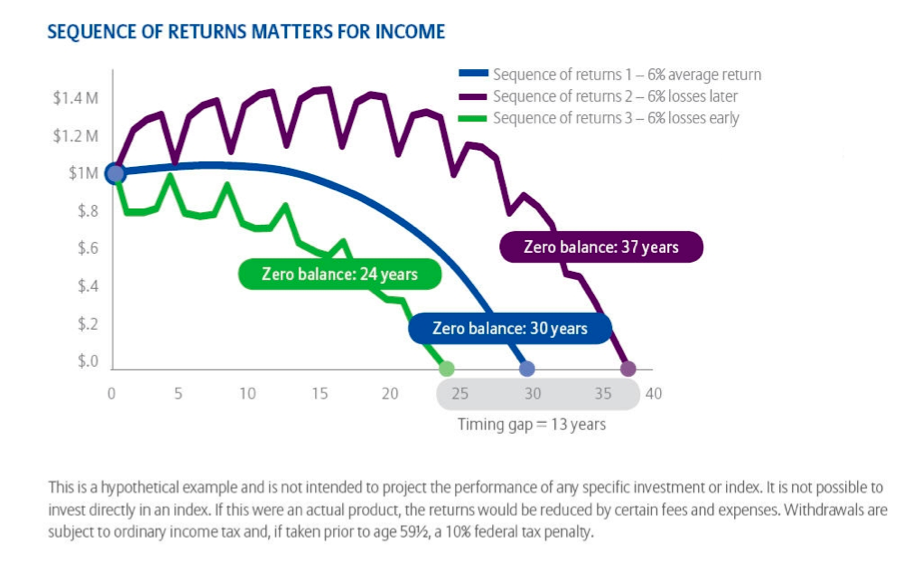

Here’s the fundamental issue: retirement is a withdrawal problem, not a return problem. When you’re accumulating wealth, volatility is mostly noise. A crash in your 40s is inconvenient, but it’s not catastrophic. You keep working, keep contributing, maybe even buy more shares while prices are down. However, once you’re retired and taking income from your portfolio, volatility becomes a structural threat. This is known as sequence-of-returns risk, a concept widely discussed in retirement literature. In simpler terms, it’s not just the average returns that matter, but the order in which those returns occur once you start withdrawing income.

If you have to sell stocks to cover expenses during a downturn, you’re locking in losses permanently. Those shares don’t recover because you no longer own them. This is what makes losses in early retirement so devastating. A market crash in year two does more damage than the same crash in year twenty. Average returns matter less than when returns happen once you’re taking income.

Then there’s the behavioral gap that the math can’t model. The 4% rule assumes you withdraw mechanically, like a machine. But people respond to fear. Continuing to withdraw your planned amount during a 30% market drop can be risky for retirees because the timing of withdrawals, combined with market losses, may shorten how long your savings last. Real people see their account balance cut by a third and panic. I have seen this a number of times in my practice, most recently during the 2020 COVID crash and the 2022 double-down year (where stocks and bonds both lost ground at year-end).

The point is: the spreadsheet assumes calm, but real life rarely is. Here, cognitive biases like loss aversion and availability bias come into play, influencing decisions. Research by Kahneman and Tversky (1979) demonstrates that loss aversion can make the fear of losing money outweigh the comfort of making informed choices, while availability bias can amplify panic by making recent market dips feel more terrifying.

Even if you stay disciplined, you still feel the stress. Your advisor says ‘stay the course,’ but you’re watching the balance shrink while bills keep coming. The 4% rule works best when people behave least like people. The first step in managing these biases is simply knowing they exist. That’s not a criticism, it’s just an acknowledgment that human beings don’t live in spreadsheets.

Now let’s talk about taxes. The 4% rule is typically modeled on pre-tax returns. But in real retirement, every withdrawal has tax consequences. If you’re pulling from a traditional IRA, that 4% withdrawal isn’t actually 4% that can be spent on your lifestyle. It’s 4% minus your tax bracket. Imagine it this way: for every $1 you withdraw from your IRA, only about $0.78 is left to pay for groceries if you’re in the 22% tax bracket. A $40,000 withdrawal at 22% shrinks to $31,200 in actual spending power.

Then there are required minimum distributions forcing income whether you need it or not, potentially triggering Medicare premium surcharges. Social Security taxation, where thresholds haven’t changed since 1983. Capital gains, dividends, state taxes. A 4% withdrawal rate before taxes is not the same as a 4% lifestyle withdrawal rate. The rule assumes taxes are secondary, but in practice, they’re structural.

So why do people cling to the 4% rule? Because it provides certainty where none actually exists. It turns an impossible question into a simple calculation. It delays harder conversations about what you actually need, about how much risk you’re exposed to, about what happens if the future doesn’t look like the past.

The rule feels objective, even scientific. It feels safer than admitting that retirement planning is more art than math, more about structure than formulas. But the rule doesn’t reduce uncertainty; it hides it. That false sense of precision is comforting in the short term, but dangerous if it prevents you from building something more resilient.

Here’s what actually breaks down in practice. You retire when markets are high, only for them to crash in year two. Suppose your portfolio begins with $1,000,000 and you withdraw 4% ($40,000) in the first year. If, in year two, the market crashes by 30%, your portfolio would be reduced to $672,000. Continuing to withdraw the same $40,000 means your withdrawal rate jumps to 6%.

You are forced to rely on those same withdrawals to cover living expenses despite the downturn. Or inflation spikes—not 2-3% but 7-8%—and your $40,000 now needs to stretch further, but your portfolio isn’t keeping pace. Or tax laws change, and your effective withdrawal rate becomes 5-6% after all the hits you didn’t model. Or you live to 95 instead of 92, and the 30-year assumption falls apart.

None of these invalidates the math. They simply overwhelm it. The rule is built for an average retirement in an average market with average behavior. Real life is none of those things.

So maybe the better question isn’t “How much can I withdraw?” Maybe it’s “Which dollars must keep working no matter what?”

This is a fundamentally different approach. Instead of building one portfolio and hoping you can withdraw sustainably, you separate your money by purpose. Some money covers essential expenses with certainty—groceries, utilities, and insurance. This money shouldn’t depend on the market cooperating. For example, a retiree might allocate funds to a guaranteed income vehicle, such as an annuity or a laddered bond portfolio, to provide predictable payments for these needs. Other money grows over time, funds discretionary spending, and builds legacy. This money can handle volatility because you’re not forced to touch it during downturns.

When you separate income needs from growth capital, you reduce reliance on market timing for necessities. You allow volatility where it’s survivable—in the growth portion—while removing it where it’s catastrophic. The problem isn’t spending 4%, it’s depending on the market to cooperate while you do.

A more durable framework starts with income stability, not withdrawal rates. How much guaranteed income do you need to cover non-negotiable expenses?

Social Security, pensions, and income sources create a floor that markets can’t shake. Then you build growth on top of that floor. The invested money can actually be more aggressive because you won’t panic and sell during crashes. You don’t need it this year, or next, or possibly for a decade.

This approach prioritizes flexibility over precision. Instead of claiming exactly 4% is safe, it acknowledges uncertainty and builds buffers. Some years you spend more, some less. The goal isn’t mathematical optimization, it’s resilience. It makes fewer assumptions about market returns, rational behavior, stable taxes, or precise longevity. It’s designed to survive even when assumptions break.

The 4% rule isn’t wrong. It’s just incomplete for how retirement actually unfolds. The math fits when the assumptions hold, but falters when life disrupts the equation.

Retirement doesn’t happen in a controlled environment. It happens in a messy world where markets crash at the wrong time, tax laws change, inflation spikes, and human beings make emotional decisions under stress. “Math meets mess,” as the saying goes, a reminder that precision on paper often melts into unpredictability in practice.

Retirement doesn’t fail on spreadsheets. It fails in the space between fear and necessity: when you need money but the market is down, when you’re supposed to stay disciplined, but you’re terrified, when the rule says one thing but reality demands another.

The goal isn’t to withdraw efficiently. It’s to live confidently. And confidence doesn’t come from a percentage. It comes from knowing that the things that matter most aren’t dependent on whether the market had a good year.

What’s the biggest assumption in your current retirement plan—something you’re hoping will be true, but can’t control? Remember how we calculated that 4% on the back of a napkin, envisioning a simple path forward? I want to hear what’s actually keeping you up at night. Reply to this email and let’s draw a clearer picture together.